What Are PropAMMs, and Why Do They Matter?

On-chain market makers that quote at CEX-grade spreads. How they work, and why they only run where repricing is cheap and fast enough.

At POL we study DeFi market structure, and this post is part of that ongoing research. The mechanisms and numbers are sourced from public data and the teams’ own docs.

Given the buzz PropAMMs have picked up, I’m going to borrow a few minutes of your time (I’ll pay you back with yield, don’t worry) to explain what these (new, at least on Ethereum) venues are, how they work, what advantages they have over traditional AMMs, and above all I’ll try to explain as clearly as I can (because it’s not that intuitive) what has to happen on the blockchain hosting them for them to be viable.

PropAMMs in one sentence

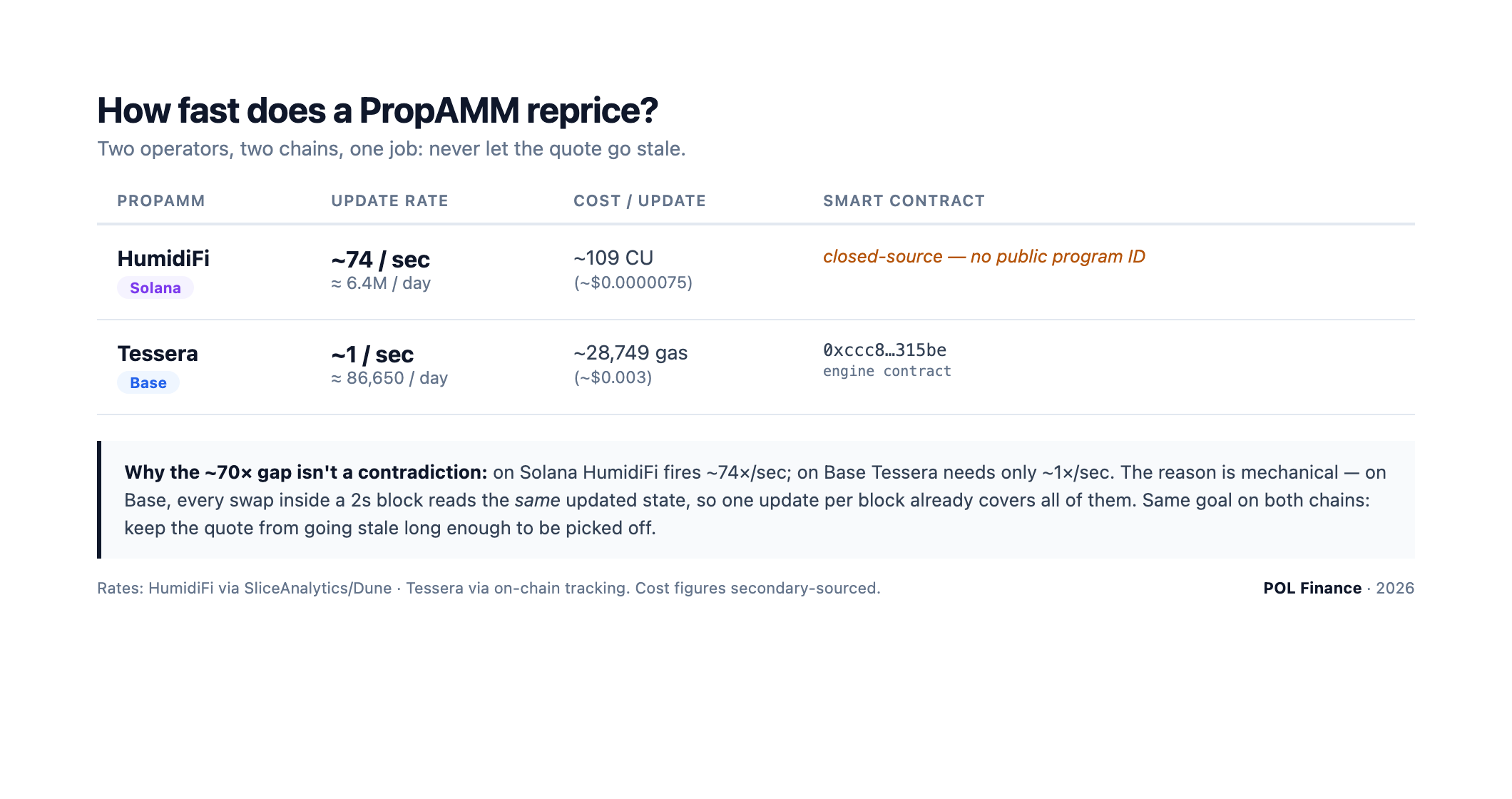

PropAMMs are decentralized markets that, unlike an AMM (where the price curve and its parameters are fixed and liquidity only updates trade by trade), have an owner. The liquidity still lives deployed in a smart contract that holds the price-formation logic (the on-chain execution program), but the owner is the one sending frequent updates to that contract to keep its price from going stale, using a private price-discovery mechanism (the off-chain pricing engine). For example: if the last price a PropAMM posted for ETH was 2000.50usd, the PropAMM’s owner should update its price again so it doesn’t get arbitraged (toxic flow).

Because the owners of these markets are the only ones responsible for their liquidity and price updates, they’re generally more sophisticated players than the typical passive LPs of an AMM. That lets the spread they offer be CEX-grade, far more competitive than an AMM’s. To get a sense: across 20M fills in March 2026 on Solana, the median PropAMM SOL/USDC fill landed 0.72 bps from the best CEX midpoint, and ~92% of fills beat the best CEX fee tier, with spreads recorded between 0.33 and 1.36 bps (PropAMMs and the Next Chapter of Permissionless Market Structure), and on Base around 2 bps (PropAMM Shenanigans). On Ethereum, Titan Builder made PropAMMs possible about a month ago, and according to Gattaca’s dashboard some pairs already quote tighter than Binance and Uniswap, which means that a PropAMM can quote tighter than both a centralized exchange and the largest on-chain AMM at once (it’s really interesting how these guys pulled it off ; I tell you about it here [LINK]).

Finally, because the liquidity lives on-chain it gets the much-wanted extra benefit of composability (i.e. other platforms and smart contracts can operate against the PropAMM’s liquidity instantly), which isn’t possible with, say, RFQs (forgot what those are already? fine, fine, go to this post and come back).

Why didn’t they exist on Ethereum?

The main financial risk of offering any on-chain pricing mechanism (financial, because the main risk is getting hacked) is keeping your price from going stale and ending up funding arbitrageurs’ profit with your own liquidity. In AMMs this cost is usually called LVR (loss-versus-rebalancing; the name comes from how you compute it: by replicating, on a CEX, the rebalancing that happens in the AMM pool). So, to guarantee fresh prices, owners have to update the parameters and the price curve as often as possible. This idea of “updating often” carries two constraints that Ethereum didn’t meet and Solana and Base do.

First, the parameter/curve update has to be cheap. Back-of-the-napkin math: if you look at how fast the bid-ask quotes refresh on Binance (the biggest CEX) for a liquid asset like ETH, it’s at least ~2 times per second. And that’s slow when you consider high-frequency trading works in milliseconds.

Second, the block time translates into the exposure the owner takes to price movement. Exposing your price curve for 12s is not the same as for 2s, or, even better, for ~400ms.

For completeness, a consequence of the first point, because if you can secure this property you can also have PropAMMs (in fact it’s what Titan Builder achieved): ordering. When the owner submits an update, if some taker had already decided to trade against the PropAMM, the update should enter the block before the taker’s tx. Otherwise the owner would be trading on old parameters. One way to secure ordering is by brute force: firing as many updates as possible. That’s cheap enough on Solana and Base, but not on Ethereum L1, where each update is too expensive, which is exactly why Ethereum needed a different solution.

Solana and Base solved these problems with different approaches.

Solana, thanks to measuring gas in compute units (CU), how cheap an update is vs a swap, and its ~400ms blocks, makes price-update rates of 74 updates/sec possible (HumidiFi, data from @SliceAnalytics). To bring it down to earth: on Solana a PropAMM update can be as cheap as ~109 CU (Wintermute) vs a Jupiter-routed swap at ~100,000 CU, roughly a 1000:1 ratio. Cheap update (price never stale) → a low fee still buys a high fee-per-CU → builders put it at top-of-block → the update lands before any taker swap can pick it off (ordering) → repeat the cycle every ~400ms (small exposure window).

Base, thanks to absolute per-update cost ~200–500× lower than L1 (~0.003 vs 0.92 for a Tessera-shape update at typical Base / L1 base-fees), its 200ms flashblock structure, and a single sequencer with cheap priority fees, allows rates of ~86,650 updates/day ≈ 1/sec (Tessera). On Base the update:swap ratio is actually similar to L1 (~1:7), it isn’t what’s doing the work.

On the EVM a single storage write costs ~22,100 gas (zero→non-zero) or ~5,000 gas (non-zero→non-zero) via SSTORE, while a swap is ~200,000–300,000 gas. So the EVM update-to-swap ratio is only ~10x, not ~1000x. That smaller gap is exactly why the “update-lands-first” trick that works for free on Solana and Base doesn’t come for free on the EVM.

On the EVM a single storage write costs ~22,100 gas (zero→non-zero) or ~5,000 gas (non-zero→non-zero) via SSTORE, while a swap is ~200,000–300,000 gas. So the EVM update-to-swap ratio is only ~10x, not ~1000x. That smaller gap is exactly why the “update-lands-first” trick that works for free on Solana and Base doesn’t come for free on the EVM.

Now that we have a notion of what PropAMMs are, how competitive they are on the chains that birthed them (Solana and Base), and the main hurdles Ethereum had to clear, I invite you to read the next blog / personal notes on the DeFi revolution led by Titan Builder [LINK].