PropAMMs on Ethereum: Beating the 12-Second Staleness Problem

How a top builder uses its vertical integration to deliver on-chain, CEX-class execution, without the LVR and ordering problems that block standard PropAMMs on L1.

At POL we study DeFi market structure, and this post is part of our ongoing research on how PropAMMs are arriving on Ethereum via Titan. The mechanisms and numbers are sourced from public data and Titan’s own docs.

Last updated: 8 Jun 2026. This is a live, fast-moving topic; running changes are logged under Updates at the end.

In a previous post we saw that PropAMMs need the curve/parameter update to be as fast and cheap as possible, so the owner is always offering the latest price it’s willing to make a market at. Solana and Base made this possible because the update is so cheap they can fire at ~1 update/sec. But the Titan Builder team solved the problem in a very practical way.

What is Titan Builder?

Gattaca is the team behind Titan Builder, one of Ethereum’s largest block builders; the PropAMM product is their bet to bring continuously-requoted (proprietary-AMM) liquidity onto Ethereum L1.

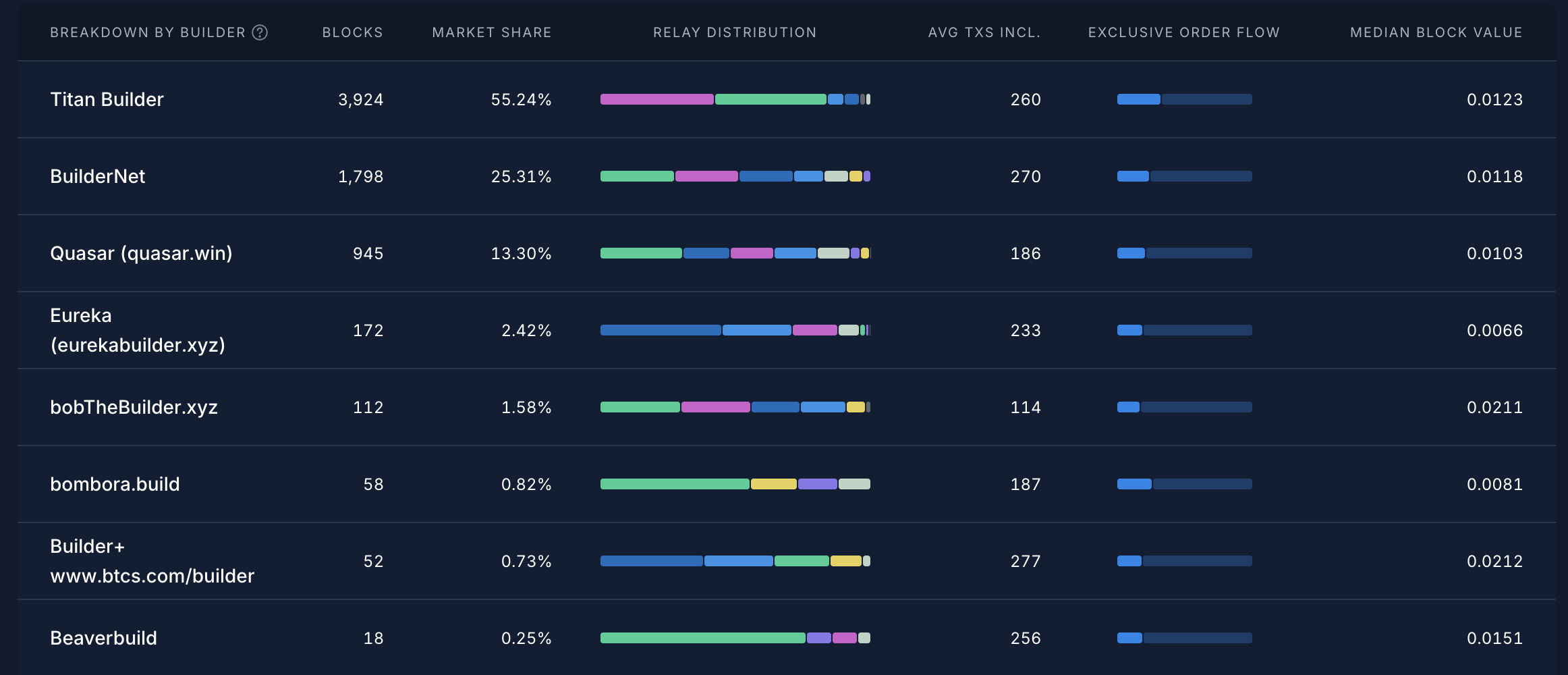

Titan Builder is their flagship builder, and today it builds more than half of all Ethereum blocks (~55%, rated.network 1-day window: the #1 builder, ahead of BuilderNet ~25% and Quasar ~13%). That puts them in a position to understand, at a very low level, how every part of a transaction’s lifecycle works, from the moment a user sends it to the moment the block is built.

That know-how and reach give them a degree of control (ugly word, but I’m using it in the good sense, I promise!) over how transactions get ordered.

That know-how and reach give them a degree of control (ugly word, but I’m using it in the good sense, I promise!) over how transactions get ordered.

What did they come up with?

Basically, they built a methodology to guarantee that takers trade against the latest update the maker sent. Titan assures the maker that its latest update will appear in the block immediately before the matching taker, the tx that’s going to trade against it, and therefore assures the taker that it always trades against the best available price.

When Titan wins the block, it controls inclusion order: it can guarantee the maker’s update lands before any taker swap in the same block. This sidesteps the public-mempool / MEV-Boost problem. (Normally on Ethereum, transactions sit in a public mempool and the block is sold to the highest-bidding builder via MEV-Boost, the marketplace where validators auction off building their block: specialized builders compete to assemble the most valuable block, and the validator takes the highest bid.) So normally a maker’s update and a taker’s swap land in an open auction, and the maker can’t be sure its update is sequenced first. Titan, building the block itself, simply places the update ahead of the swap. The maker doesn’t have to defend in an auction; the builder just orders the update first.

Advantages and disadvantages

All these extra features point at one target: shrinking the maker’s adverse-selection window, the gap in which an informed taker can pick off a stale quote. The smaller that window, the tighter the maker can afford to quote (the same LVR cost from the last post, now actively defended against).

-

Takers can submit a bundle of alternative routes for the same trade. When Titan builds the block, it checks whether the target maker really offers the best route versus the submitted bundle; if not, it executes the best route in the bundle. These alternative routes (including a CFMM fallback) also cap how far the maker can widen at the last moment: if the maker re-prices too aggressively, a CFMM candidate wins the trade instead. That’s what keeps a “quote tight to win, widen at fill” move (spoofing) in check. There’s a real wrinkle in how this committed/captive flow gets priced, which I’ll unpack in a future post. 👀

-

Makers are protected against toxic flow trying to exploit stale prices via a delay

bbetween a taker’s tx and the maker’s latest quote. For example, withb = 50ms, an update received at time T can only be matched against takers received before T−50ms (i.e.taker_recv + b < quote_update_recv). Makers can also opt for conditional inclusion: the quote-update tx only lands on-chain when a taker actually trades against the pool; quotes nobody hits never get posted. (Different knob fromb:bdecides which takers may match a quote; conditional inclusion decides whether the quote tx is published at all.) -

Searchers, solvers and DEX aggregators can connect to a stream of the latest pAMM states, for the makers who opt to publish theirs.

Put together (ordering + freshness b + conditional inclusion + re-simulation until inclusion), the price a taker hits is milliseconds-stale instead of up-to-12-seconds-stale. That collapsed window is the whole reason an Ethereum PropAMM can quote near CEX levels.

Like everything, the system has its limits:

-

It’s not trustless end-to-end: quote delivery and ordering sit at the builder (off-chain trust in Titan and other builders that have and will incorporate this feature). Critics frame it as “a sidecar to the block-building pipeline, more like an integrated RFQ.”

-

Committed flow + the maker’s last look create a free option: quote tight to win the route, then re-price toward the taker’s slippage limit. The router caps it, but it’s a real open weakness.

-

It leans on one dominant builder, which sits uncomfortably with Ethereum’s decentralization, which is why Titan is exploring making the guarantee permissionless and builder-agnostic, e.g. via the Flashbots priority-update-registry (per their own Makers docs), so the freshness edge wouldn’t depend on a single builder winning the block.

-

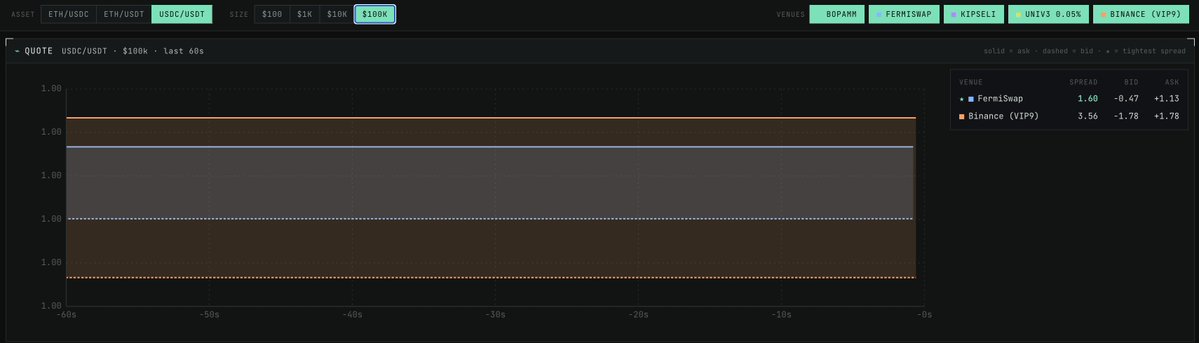

The pricing edge is conditional: it shrinks as trade size and volatility rise. On large volatile fills (e.g. $100k ETH/USDC) Binance’s deep, netted book still wins; the repricing-speed advantage only dominates when inventory risk is low (stable pairs) or size is moderate.

Is it really on-chain, or an RFQ in disguise?

A fair objection raised on Twitter: if the freshness guarantee lives at the builder, isn’t this just an off-chain RFQ with extra steps? Partly: the quote streaming and the ordering guarantee are builder-mediated, and they only hold in the blocks Titan actually builds. But the part that matters is on-chain: the pAMM is a real Ethereum pool you can swap against directly, with no off-chain matching layer, and once the update lands a swap settles like any other AMM, fully composable into solver, arbitrage and aggregator routes. So it’s an on-chain composable AMM with a builder-enforced freshness guarantee, not an off-chain RFQ, but that guarantee is only as wide as Titan’s block share.

How competitive is it, really?

Per the real-time data on Gattaca’s dashboard, these PropAMMs already compete with, and for some sizes beat, Binance and Uniswap v3.

On tight, stable pairs the PropAMMs are hard to beat: for a $100k USDC/USDT trade, FermiSwap quotes 1.60 bps vs Binance’s 3.56, more than 2× tighter.

On ETH/USDC they’re very competitive at small-to-mid size: at $1k, FermiSwap (2.00) and Kipseli (2.31) both beat Binance (3.51); at $10k they trade blows, and in every case they sit far inside Uniswap v3 (~10–20 bps). But push size up on a volatile pair and it flips: at $100k ETH/USDC, Binance wins (6.81) while FermiSwap widens out to ~10. So the edge is real but conditional, tightest where the asset is stable, weakest on large, volatile trades.

And volume is climbing fast: daily PropAMM volume hit ~$22M on Jun 5 (partial) and was projected to close ~$31M (per LambdaClass / Fede’s intern, Jun 6), up from sub-$1M/day a week earlier. (These figures move daily; treat them as a dated snapshot, not a fixed level.)

Updates

-

11 Jun 2026: FermiSwap quotes 0.40 bps vs Binance’s 3.56 bps for all trade size in USDC/USDT.

-

6 Jun 2026: $100k ETH/USDC PropAMM spread widened to ~30 bps (Binance ~8); large-volatile pricing is proving erratic (was ~10 bps on Jun 4). Daily PropAMM volume ~$2M (partial), projected ~$31M.

-

4 Jun 2026: Added USDC/USDT $100k data (FermiSwap 1.60 vs Binance 3.56) and the conditional-edge framing: tight on stable pairs / moderate size, weak on large volatile trades.