Why Are There So Many Ways to Trade Crypto? A Map of DeFi Venues

The CEX/DEX/AMM/PropAMM/RFQ/aggregator map I wish I'd had when I started.

The DeFi universe is confusing. When I first started reading about this stuff, I had a hard time sorting out what kinds of platforms even exist. Why would I ever leave the comfort of Binance? This post is the map I wish I’d had back then.

It’s current as of today, but like any new blockchain tech, it won’t be long before it’s outdated again. Still, as of now it covers all the venues where you, the user (aka the taker), can go buy or sell assets (aka trade) against a counterparty (aka the maker) who provides the funds and the price-formation mechanism that makes the trade possible.

We’ll look at CEX vs DEX, and inside the messy DEX world we’ll cover AMMs, PropAMMs, PMMs (via RFQ/RFS), and aggregators. That last one isn’t strictly a price-former in the sense above, but aggregators are still a vehicle for trading, so for completeness I’ll cover them too (I’ll probably do a dedicated post on that world another time; it has several moving parts and names: aggregator, meta-aggregator, router, solver).

CEX vs DEX

Let’s start with the split between the two big groups of platforms where users can operate.

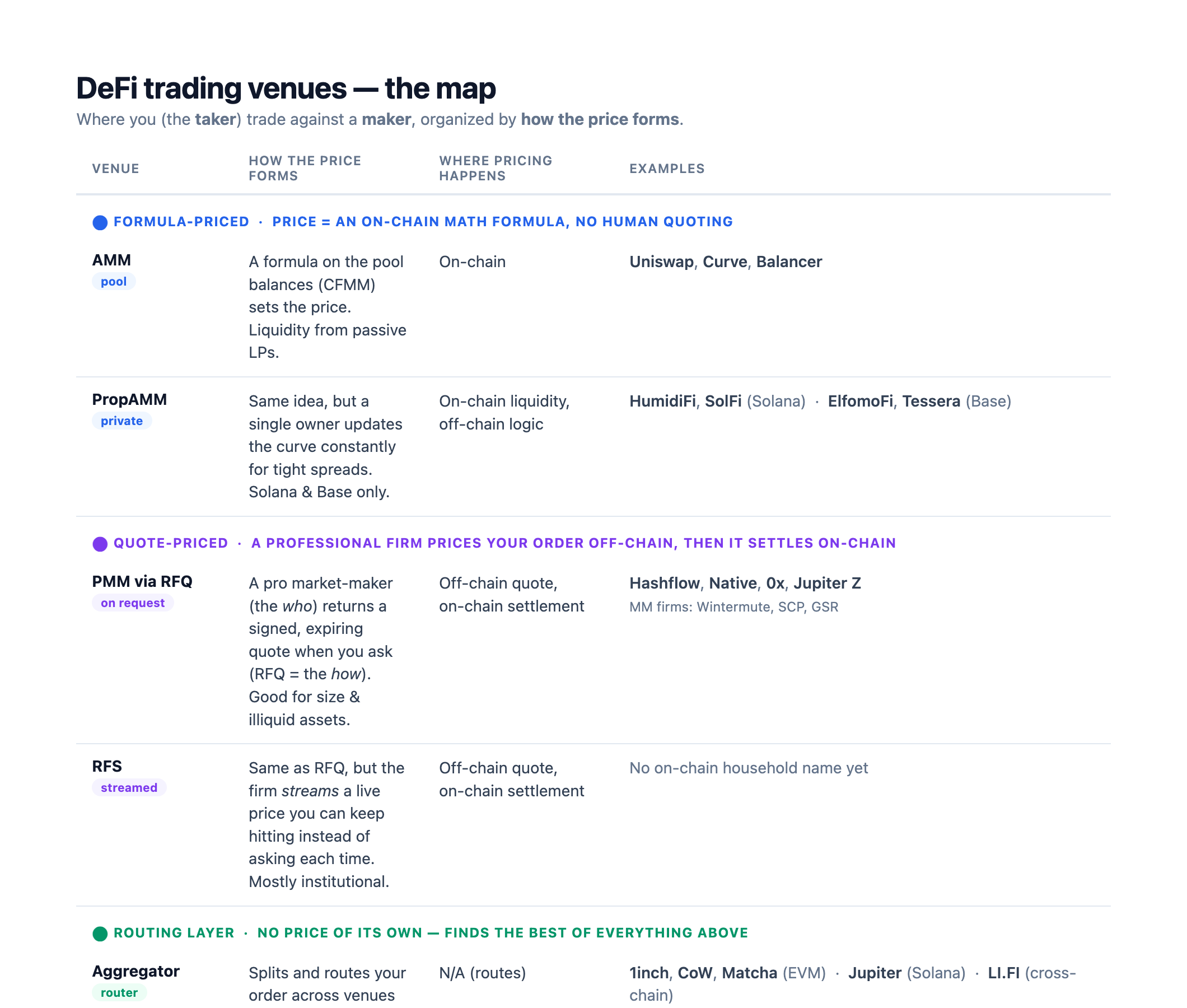

-

CEX (Centralized Exchange). As the name says, it’s a centralized trading platform: there’s a company (or group of companies) that owns it. For the less-informed user it ends up being an easy, friendly, fast way in, through well-known platforms like Binance, Coinbase, or Ripio (the more degen users, the ones more clued-in to what blockchain offers, tend to go elsewhere). But the fact that there’s an owner means the platform holds your private keys and your crypto, not you. They also usually require identity verification (KYC). One extra upside: you can operate with fiat currencies.

-

DEX (Decentralized Exchange). These appeared as a fully decentralized answer to the same need: buying and selling crypto assets. As the name says, and unlike CEXes, there’s no owner; instead the rules for exchanging crypto are written into the code of the smart contracts that define them. The upside: you own your assets and the private keys to operate, and you don’t need any KYC. The flip side: the risks generally include potential hacks, often less competitive prices (at least on passive AMM pools), and extra complexity when using them.

The DEX world, in 3 buckets

Now, the DEX world has its nuances, because the smart-contract rules vary. Depending on the type and sophistication of the end user, and the asset being traded, there are many platforms and many different logics. In my head I sort them into 3 groups, by the underlying price mechanism:

1. Formula-priced

Platforms where the price emerges from a closed mathematical formula. These include:

-

AMM (Automated Market Makers). These work thanks to an automatic price-formation mechanism based on the quantity of each asset in the venue. You find liquidity pools holding 2 or more assets; each asset has a concrete balance in the pool, and the price forms by applying a math formula to those balances. Another generic name for them, tied to that formula, is Constant Function Market Maker (CFMM). Depending on the asset type (stablecoins or volatile assets) and its liquidity, the formula varies and can be as sophisticated as you want. The best known are: Constant Product (x·y = k, the price comes from the product of the balances) like Uniswap; Constant Mean ( · = k, the price comes from a weighted geometric mean, a+b=1) like Balancer; and Hybrid Function (which combines Constant Product with something called Constant Sum, which keeps the pool from emptying out while giving a better price for highly correlated assets like stablecoins) like Curve. Other names on Solana: Raydium, Orca.

-

PropAMM (Proprietary AMM). It’s an AMM, but with an owner. The rules and the liquidity are defined and updated by the owner of the smart contract. The logic is similar to an AMM in that the price comes from an algorithm with automated rules, but the parameters and the calculation rules are private. You can interact with them directly if they have an API or a frontend, or through an aggregator (see below). Because they need on-chain liquidity and a competitive price at all times, PropAMMs don’t exist on Ethereum as standalone on-chain venues; the only Ethereum case is builder-mediated (Titan), which is exactly what the next post is about. PropAMMs live on Solana and Base (see this post, where I go into why they exist only on those chains [LINK]). Examples on Solana: HumidiFi, SolFi, Obric; on Base: ElfomoFi, Tessera.

2. Quote-priced

This bucket groups the platforms where pricing happens off-chain, as a response to a request from the user (or from the go-between connecting the market maker and the user). These fall here:

-

RFQ (Request for Quote). As the name says, these are off-chain providers that quote prices when a user sends a buy or sell request for a certain amount. Usually the user doesn’t connect to them directly; instead, there’s a platform that acts as the go-between between the user and the RFQ. Typically you reach one of these platforms, send your trade request, and the platform routes it to all the connected market makers so they compete to offer the best price; once the best price is chosen, the platform reports it back to you, and you decide whether to accept.

-

RFS (Request for Stream). It’s an RFQ, except instead of answering each request with a one-off quote, the provider responds with a continuous stream of prices over a time window.

-

PMM (Private / Professional Market Makers). These are the professional players that compete inside the RFQ for the user’s trade: specialized pricing firms that answer quotes by looking at their own books.

In short: the firm is the PMM, and you reach it via RFQ or RFS. Some RFQ venues: Hashflow, Native, 0x, Jupiter Z (Solana). The MM firms behind them: Wintermute, SCP, GSR. There’s no on-chain RFS today; it’s mostly institutional / off-chain.

3. Routing layer

Technically these aren’t platforms with their own price-formation rules. Their job: given a buy or sell order for some asset (sent by a user via a frontend), the aggregator computes the route that gives the best price (in terms of how much of the asset you actually end up receiving) across the venues we mentioned above (both CEXes and DEXes). Some even search across other chains (multi-chain), operating through bridges. Among the best known: 1inch, CoW Swap, Matcha (same-chain), LI.FI, RocketX (multi-chain); Jupiter (Solana, the big one), and Titan (Solana). There are also interest-rate aggregators, but they’re out of scope for this mini-post.

What’s next

Right now something interesting is happening on Ethereum: the recurring noise is that PropAMMs are starting to arrive on the network. This post is just a quick intro to the different ways you can trade crypto assets, but the PropAMM case is especially interesting: it offers much more efficiency and a much better user experience than passive AMM pools. So how do PropAMMs actually work, and above all, why do they exist on Solana and Base but not (yet) on Ethereum? I’ll go deeper in the next post [LINK].

Further reading

-

AMMs / CFMMs: Uniswap, constant-product (uniswap.org) · Curve, StableSwap for pegged assets (curve.fi) · Balancer, weighted pools (balancer.fi)

-

The math behind CFMMs: Angeris, Kao, Chitra et al., An Analysis of Uniswap Markets (2019), https://arxiv.org/abs/1911.03380

-

Aggregators: 1inch (1inch.io) · CoW Swap (cow.fi) · Jupiter, Solana (jup.ag)

-

RFQ / PMM venues: Hashflow (hashflow.com) · 0x (0x.org)

-

Next in this series: What Are PropAMMs, and Why Do They Matter? [LINK]